Call/text: (702) 906-0389

This week, our National Association of Realtors released their report titled "Existing-Home Sales Suffer Setback in November, Fall to Slowest Pace Since April 2014"

The report stated:

"Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, fell 10.5 percent to a seasonally adjusted annual rate of 4.76 million in November (lowest since April 2014 at 4.75 million) from a downwardly revised 5.32 million in October. After last month's decline (largest since July 2010 at 22.5 percent), sales are now 3.8 percent below a year ago — the first year-over-year decrease since September 2014."

The report triggered a series of articles in the news questioning whether the housing market is slowing. We had numerous calls and emails from our clients with concerns about the current market conditions and how it will affect their current or planned real estate transactions.

The primary reason for the sales drop is the new mortgage regulation implemented in October, the “Know Before You Owe” rule. This mortgage rule, known as the TILA-RESPA Integrated Disclosure (TRID) caused extended time for escrow closing. The November sales were not lost, they simply were pushed in to December.

Lawrence Yun, NAR chief economist, explained: "affordability issues continue to impede a large pool of buyers' ability to buy, which is holding back sales. However, signed contracts have remained mostly steady in recent months, and properties sold faster in November. Therefore it's highly possible the stark sales decline wasn't because of sudden, withering demand."

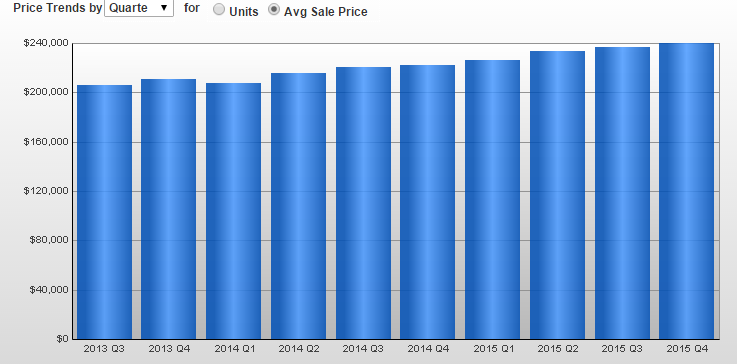

According to NAR: “The median existing-home price for all housing types in November was $220,300, which is 6.3 percent above November 2014 ($207,200). November's price increase marks the 45th consecutive month of year-over-year gains.”

Regardless of low sales numbers for November, we feel the housing market is still doing well as demand remains strong.

The challenge for buyers we are seeing are that homes that stay on the market are either not in the desired area or they are not in their price range. Limited inventory always makes it harder for the buyer since they what the most house for their dollar, in the area they wish to make a home.

The remedy...we need more houses in the inventory and priced at what the market will allow! We have the buyers, we need the inventory to match!

Seller's are still slightly overpriced, which makes it challenging for buyers when we set criteria in their price range and the right house is not in that range. Additionally, the bigger concern is the actual appraisal coming in too low and we all head back to the negotiating table.

However, the upside is the market is still stable and we see many first time buyers testing the waters. The programs available for buyers is helping them get in with less cash! With that, we are seeing less cash investors swooping in and taking homes from the regular buyers! The seller that understands where we are in the market is the one getting his house sold quickly or at the best price!

Source: National Association of Realtors, Greater Las Vegas Association of Realtors

Please enter your information to login or Sign up here.

Please enter your email and we'll send you an email message with your password.

Already have account? Sign in.

Already have an account? Sign in.