Call/text: (702) 906-0389

Whether you want to buy or rent is your personal decision based on your life situation as much as the housing market. “If this is not the time for you, there will be a time in the future, there will be a property, there will be an appropriate mortgage product... Do not try to time the market. Time your purchase around your life.”

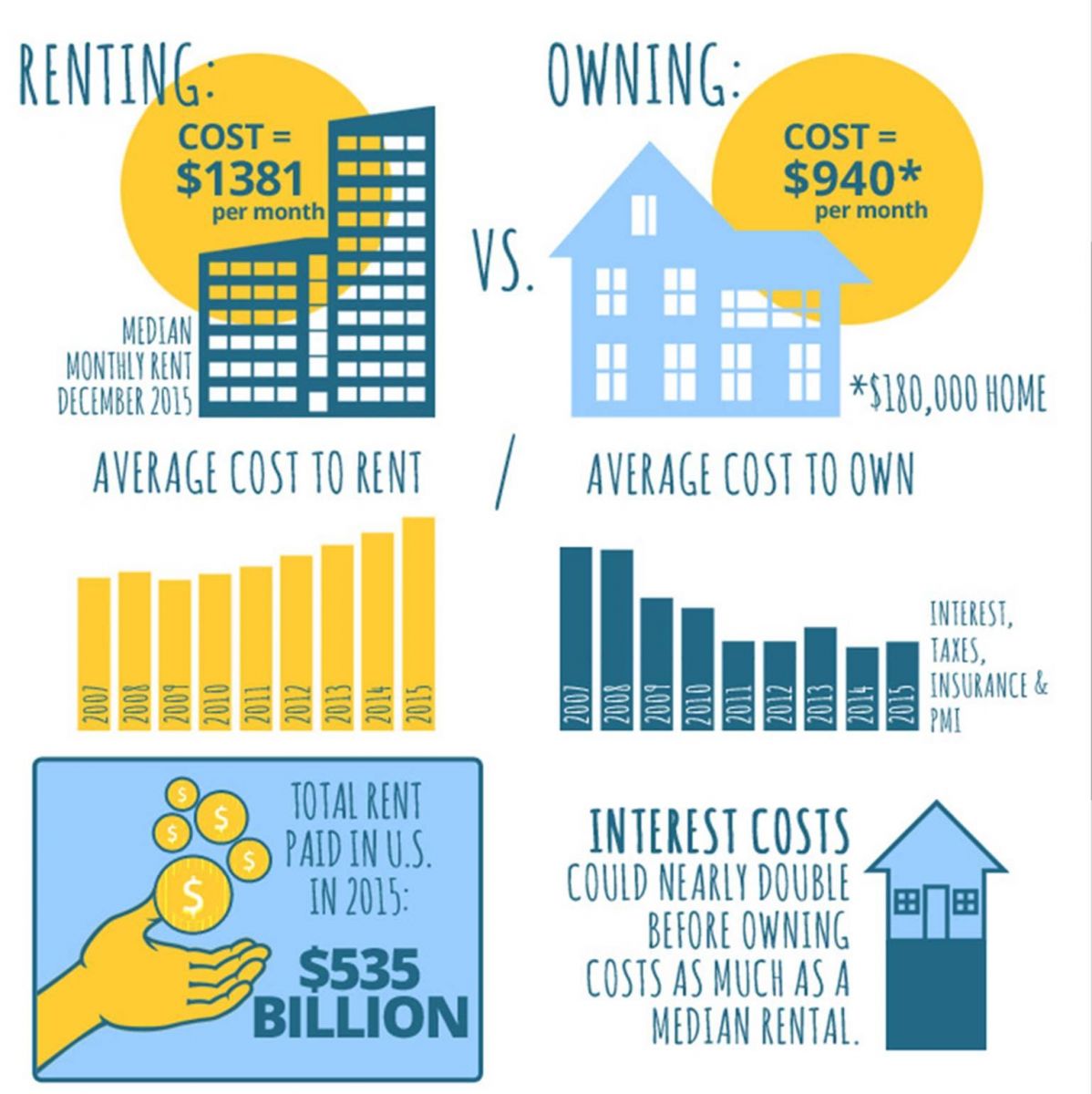

Renting a home provides you a roof over your head and the flexibility to leave when you want. At the same time, it can feel like you’re throwing money away by not building equity in your home. By some estimates, the median monthly rent cost is about 25% higher than a typical monthly cost for owning a mid-priced home. Check out these quick facts:

*Costs to own are averaged historical samples only; they are not an offer to lend. Costs as follows: historical, annualized average prevailing first year monthly interest expense for a loan amount of $162,000 (10% down on a $180,000 home), taxes of $300, insurance of $40.50, Private Mortgage Insurance of $81. Actual expenses vary for any home and loan program; will include additional considerations for principal, maintenance, potential tax savings and appreciation/depreciation; and can be more or less than illustrated. Rates and fees for current scenarios available by request. Data is provided with rights for use by Estate of Mind, Inc.

Please enter your information to login or Sign up here.

Please enter your email and we'll send you an email message with your password.

Already have account? Sign in.

Already have an account? Sign in.